{kind=link}

Uncategorized

Net Worth Update February 2021: $369,022

February's net worth update for the Money Prowess household shows no major changes from January 2021.

{kind=link}

Uncategorized

Net Worth Update January 2021: $365,247

I didn’t really do New Year’s resolutions this year, but I did whisper some goals to myself. I would like to be better about posting. I will likely fail at that goal. And fast. Anyone want to take bets? Whatever your goals, be kind to yourself Last year was a bit rough. This year may […]

{kind=link}

Uncategorized

2020 Net Worth Year in Review Update

Since my last net worth update was from April 2019, I’m going to cover where we started off financially in 2020 and where we ended up by the end of the year.

{kind=link}

Uncategorized

Net Worth Update: November 2018

Net Worth: $61,960 Stock slump got me down Whoosh! 10k in value gone from my retirement accounts in a few days. What an awesome amazing problem to have. It also doesn’t matter. Like it matters, but not to me, not right now. It would matter if I was about to take out money from my […]

{kind=link}

Uncategorized

Net Worth Update May 2018: $50,070

Net Worth Update: $50,070 I Fell Off the Net Worth Reporting Wagon for 5 Months! It didn’t seem like it’s been that long. Apparently, this is the first of 2018 and I’m totally not prepared for it to be momentous. As I said, I bought a house. And not just any house, a three family […]

{kind=link}

Uncategorized

Net Worth Update December 2017: $80,471

Net Worth Update: $80,471 Woot! Officially over the $80,000 net worth barrier. After reading the Globe piece noting median net worth in Boston ($8 for US blacks vs $247,500 for whites), it puts our position in further local perspective. We’re sooo close to have $200,000 in retirement savings alone. As the year wraps up, I’ll […]

{kind=link}

Uncategorized

Net Worth Update November 2017: $78,361

My Money Now Prints Money So Why Don’t I Feel Rich? We have entered “the zone.” Not only is a kick ass stock market helping nudge us along, but we’re generally at the tipping point that our money is printing more money. Our assets keep growing without us lifting a finger. Maybe soon we’ll be […]

{kind=link}

Uncategorized

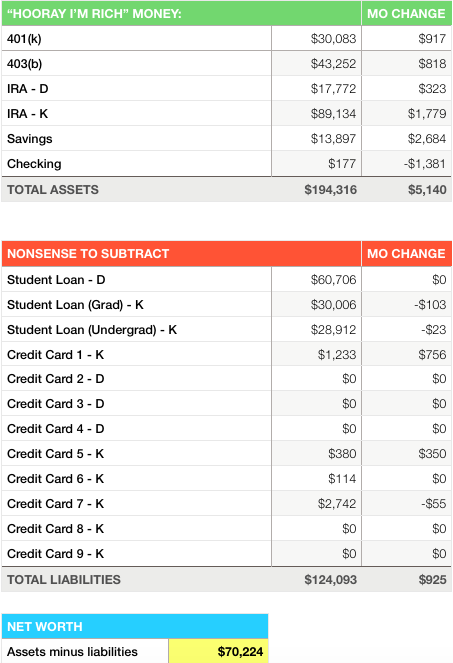

Net Worth Update October 2017: $70,224

Net Worth: $70,224 Month Change: +$4246 My growing graduate student loan continues to haunt me. 2017 Net Worth Tracker: January: $14,107 February: $21,285 March: $30,016 April: $32,939 May: $33,537 June: $38,883 July: $41,518 August: $57,943 September: $65,997

{kind=link}

Uncategorized

Net Worth Update August 2017: $57,943

Our net worth leaped up over 16k in one month! This is all due to investing in a speculative new stock that increased 10x overnight. Just kidding. That just about never happens. I finally got paid an annual performance bonus in one large lump sum. Net Worth: $57,943